Why the Sunshine Coast Property Market Is Outperforming the Nation

By Leigh Martinuzzi | Martinuzzi Property Group – eXp Australia

There’s a phrase worth retiring in 2026: “the Australian property market.” There isn’t one anymore. There are dozens of markets, all moving at different speeds. The gap between the strongest and the weakest has rarely been wider. Some capitals are setting fresh record highs. Others have quietly slipped off their peaks.

For anyone with a stake in property here, that’s the whole point. The national headline tells you almost nothing about your street. What matters is knowing where your own market sits. Right now, the Sunshine Coast sits in a strong position, even as parts of the country cool.

What the latest national figures are telling us

Growth is slowing, not reversing.

Cotality’s newest chart pack, pulled together by Michael Yardney’s Property Update, paints a clear picture. The market is still rising. It’s just slowing down.

National home values rose just 0.6% over the three months to May. That’s down from 1.6% the month before. Annual growth has eased to 8.8%, after peaking near 10% in February. This is a cooling, not a correction.Cotality’s newest chart pack, pulled together by Michael Yardney’s Property Update, paints a clear picture. The market is still rising, but it’s downshifting.

National home values rose just 0.6% over the three months to May, down from 1.6% the month before, and annual growth has eased to 8.8% after peaking near 10% in February. It’s a cooling, not a correction.

Every state is running its own race.

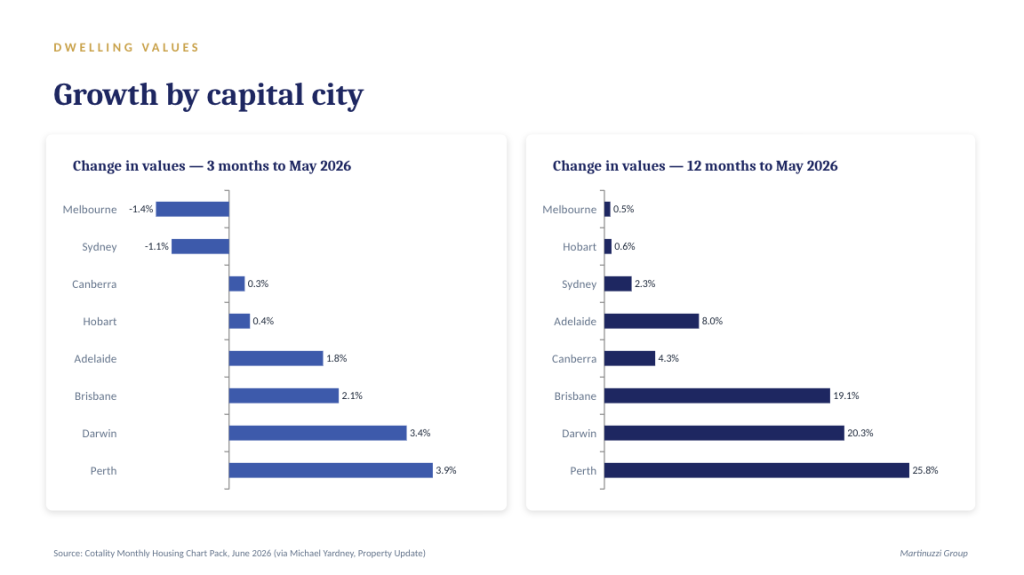

The bigger story is how differently each state is performing. Perth is up around 25.8% over the year, and Darwin about 20.3%. Both are at record highs. Brisbane isn’t far behind at roughly 19.1%.

Adelaide and Canberra are still rising. Sydney has slipped about 2.1% below its late-2025 peak. Melbourne sits around 3.2% under its 2022 high. Hobart, once the darling of the boom, is also off its peak.

The gap between the fastest and slowest capital is now about 25 percentage points. That’s why a national average means very little for any single suburb.

Lower prices haven’t meant cheaper homes.

There’s a catch worth understanding here. Prices have dipped in Sydney and Melbourne. Yet homes there haven’t become easier to afford. Interest rates are higher, so the cost of servicing a loan has climbed. That has cancelled out the price falls. The real squeeze in this market isn’t price. It’s borrowing power.

Buyers are getting a little more room.

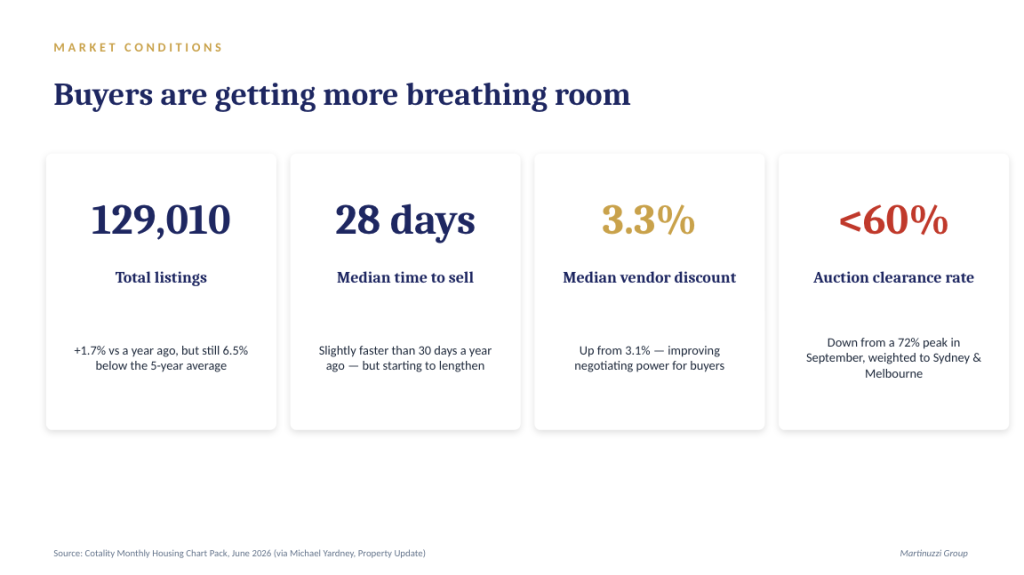

On the ground, conditions are slowly tilting back toward buyers. Total listings sit near 129,010. That’s a touch above last year, but still around 6.5% below the five-year average.

Homes are taking a median of about 28 days to sell. That’s faster than the 30 days a year ago, though selling times are starting to lengthen again. Vendor discounting has crept up to 3.3%. Auction clearance rates have slipped below 60%, down from a 72% peak last September.

None of it is dramatic. Together, though, it gives buyers a little more room to think and negotiate.

Rentals are the exception

Rentals are the one part of the market that isn’t cooling. National vacancy is just 1.5%. That’s well under the decade average of 2.5%. Rents are up 5.9% over the year.

As values cool and rents climb, yields are rising too. Gross rental yields have edged up to around 3.62% nationally. Regional markets (4.2%) are now doing better than the capitals (3.5%).

Why this isn’t a crash

Worried the slowdown points to a crash? The numbers say otherwise. As Michael Yardney put it, our housing markets face challenges from every direction, yet have “remained resilient”. The national balance sheet backs that up.

Australian homes are worth about $12.6 trillion. Mortgages against them total only $2.6 trillion. That’s a very comfortable 20% loan-to-value position nationally. Housing also holds close to 55.8% of all household wealth. It’s a big reason the banks, the government and the RBA all want to avoid a property crash.

What it means for homeowners

If you already own on the Sunshine Coast, the headline is reassuring. Years of strong local growth mean most owners are sitting on substantial equity, and the national fundamentals above suggest the broader market remains structurally stable rather than fragile.

The one area worth your attention is the higher-rate environment. If you haven’t reviewed your loan in a while, it may be worth a look, not out of worry, but simply to understand where you stand. For some households, a chat with a good broker about serviceability or refinancing could be time well spent. Knowing your numbers always beats guessing at them.

What it means for sellers

Demand here is still very much alive, but buyers have become more selective and far more conscious of what they can borrow. That changes how you approach a sale.

It means you can’t rely on the market to do the heavy lifting the way you might have a year or two ago. Pricing, presentation and timing matter more now, not less. A well-prepared, sensibly priced home still draws strong interest and can move quickly, and that 28-day median is healthy. An overpriced or underprepared one tends to sit, and a property that lingers often ends up costing more than getting the strategy right from the outset. This is a market that rewards a clear plan over hopeful guesswork.

What it means for buyers

There’s more breathing room than there was through the frenzy of 2025. In many cases you now have time to compare, do proper due diligence and negotiate, rather than feeling forced to decide overnight. That’s a healthier market to buy into.

The real constraint has simply shifted. It’s less about competition and more about borrowing capacity. With rates where they are, getting your finance sorted early isn’t just sensible. It’s what lets you act decisively when the right home appears. Good stock still moves fast, so being prepared is half the battle.

What it means for investors

For investors, the rental side of the equation is doing the talking. With national vacancy at 1.5% and yields lifting as values cool, the income case has quietly strengthened, and regional markets are leading the capitals on yield. Locally, vacancy sits near 1.1%, supporting house yields of around 4.1%, with pockets of the hinterland offering some of the more accessible entry points in the region. As always, the suburb-level numbers matter far more than the regional average, so it pays to look closely rather than buy the headline.

The local Sunshine Coast story

Here’s where our patch parts ways with the national picture. While Sydney and Melbourne have softened, South East Queensland has been one of the strongest stories in the country, and the Sunshine Coast has continued to climb with it.

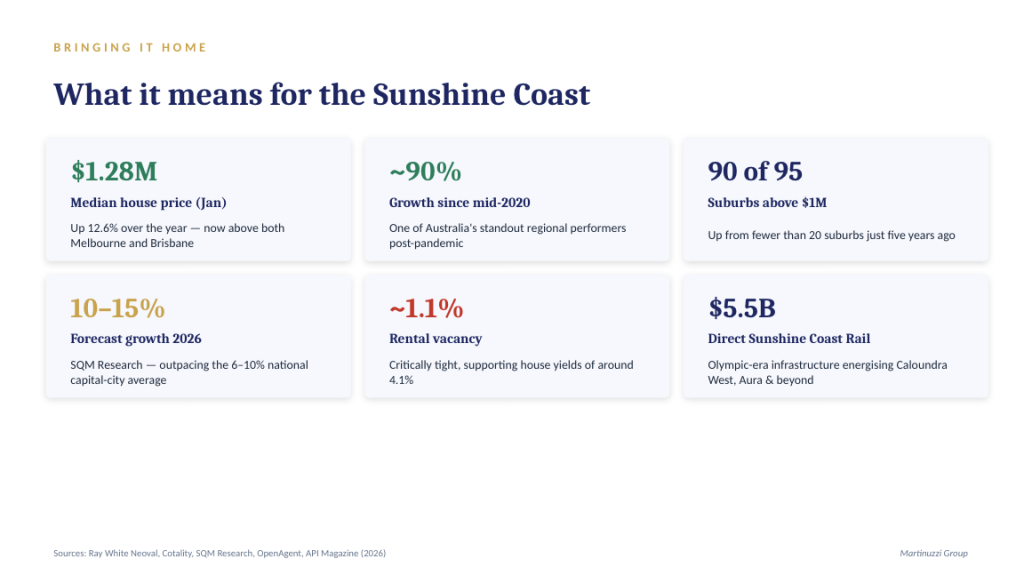

The local median house price now sits at around $1.28 million, up roughly 12.6% over the year. To put that in perspective, our median is now above both Melbourne and Brisbane, a remarkable shift for a region that, not long ago, was prized mainly for being the affordable coastal alternative. Values here have risen close to 90% since mid-2020, making the Sunshine Coast one of Australia’s standout regional performers post-pandemic.

The depth of that growth is striking. According to Cotality, 90 of 95 Sunshine Coast suburbs now carry a median house price above $1 million, up from fewer than 20 suburbs just five years ago. And the momentum is forecast to continue, with SQM Research expecting regional growth of 10 to 15% in 2026, ahead of the 6 to 10% pencilled in for the national capital-city average.

What’s underpinning all of this is no mystery: steady interstate migration, persistently tight supply, a vacancy rate near 1.1%, and a long pipeline of infrastructure investment heading into the 2032 Olympics. The $5.5 billion Direct Sunshine Coast Rail project alone is set to reshape connectivity and energise growth corridors like Caloundra West and Aura.

That said, even strong markets eventually find a more sustainable rhythm, and with our median now above Melbourne’s, affordability and borrowing capacity have genuinely become part of the local conversation, particularly for first-home buyers. It’s also worth remembering the Coast isn’t one market either. The hinterland, including Palmwoods, Woombye, Nambour, Burnside, Coes Creek, Mooloolah Valley and the smaller pockets around them, often offers relative value compared with the coastal strip, along with the space and lifestyle so many families and downsizers are chasing.

A practical next step

If you’re weighing up a move in the next 6 to 12 months, whether that’s selling, buying, upgrading, downsizing or adding to a portfolio, it may be worth getting a clear, current read on where your property sits today. A quick, no-pressure conversation can give you far more clarity than any national headline ever will, and it’s exactly the kind of guidance we’re here to provide.

Feel free to reach out anytime. I’m always happy to talk through what this market means for your situation specifically.

Request Your Free Market Appraisal Today! 👉 Click here to book your appraisal

SUBSCRIBE to stay updated with all latest property insights and news 👉 Click Here to Subscribe

The Sunshine Coast Seller’s Guide to Choosing the Right Agent 👉 Get Your Free Guide Here

Preparing for Settlement: A Seller’s Guide to a Smooth Handover 👉 Download the Guide Here