Higher Rates, Affordability Pressure, and Why Good Property Still Stands Out

By Leigh Martinuzzi | Martinuzzi Property Group – eXp Australia

Over the past week, the property conversation has become less about momentum alone and more about the tension between resilience and pressure.

From where I sit, the market is still moving, but it is doing so with more discipline. Buyers are more cautious, sellers need to be more realistic, and affordability is becoming one of the biggest forces shaping decisions right across the country. That matters here on the Sunshine Coast as well, because while our market has its own character, it is still influenced by the broader economic backdrop.

What stands out to me most right now is that property is not weakening across the board. Instead, the market is becoming more selective. Good property still stands out. Well-positioned homes are still attracting attention. But buyers are looking harder at value, finance, and long-term livability before they commit.

Rates, inflation and confidence

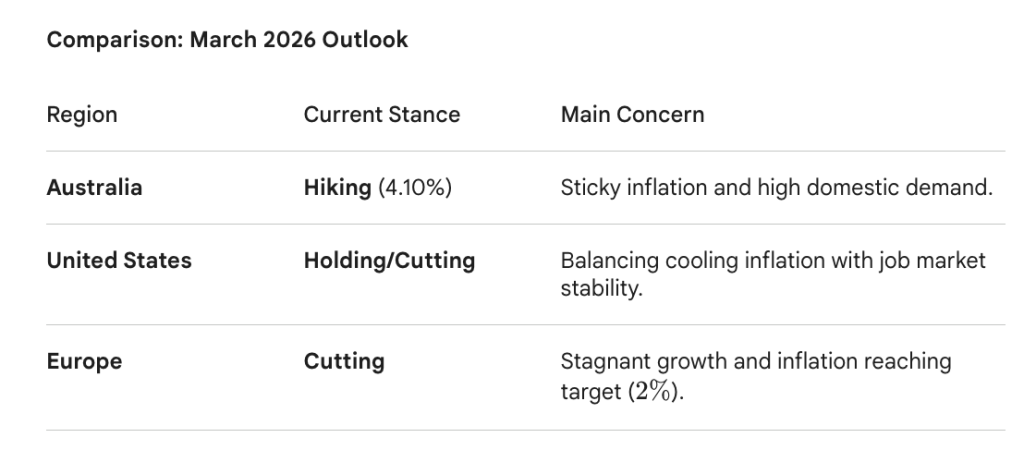

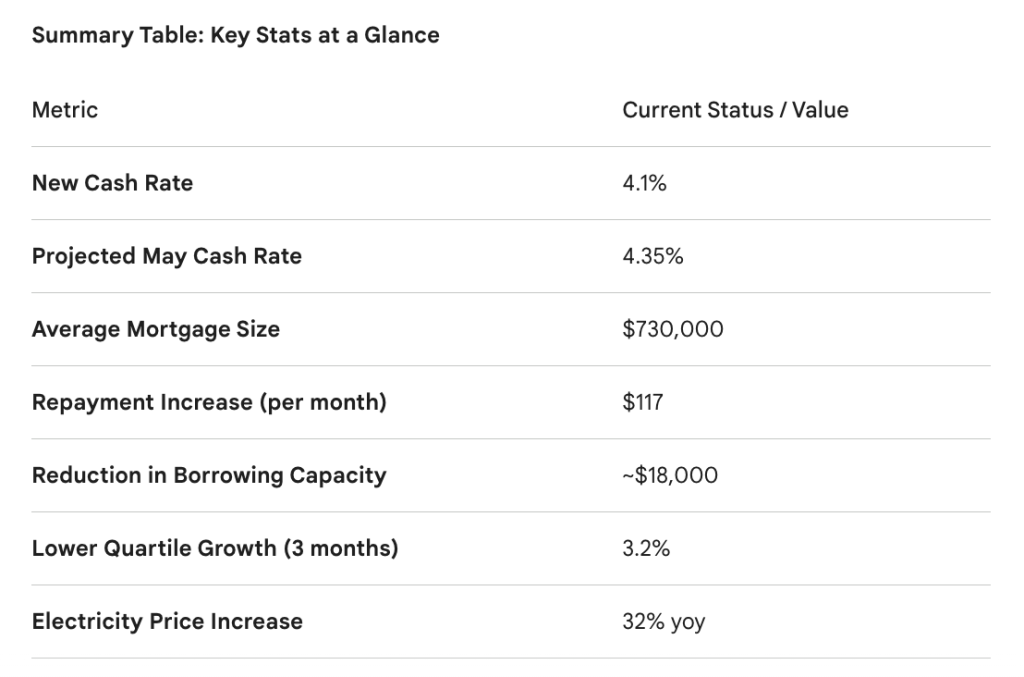

One of the clearest shifts in recent weeks has been the change in the interest rate outlook. The Reserve Bank lifted the cash rate to 4.10 per cent in March, and what I think is important here is that the decision was far from one-sided. It was a narrow 5 to 4 vote, which tells you there is real debate even inside the Bank about how much more pressure households and the broader economy can absorb.

I also think a lot of people are asking a fair question right now. Why is Australia still talking about raising rates when the US and Europe seem more in wait and see mode, or even talking about cuts?

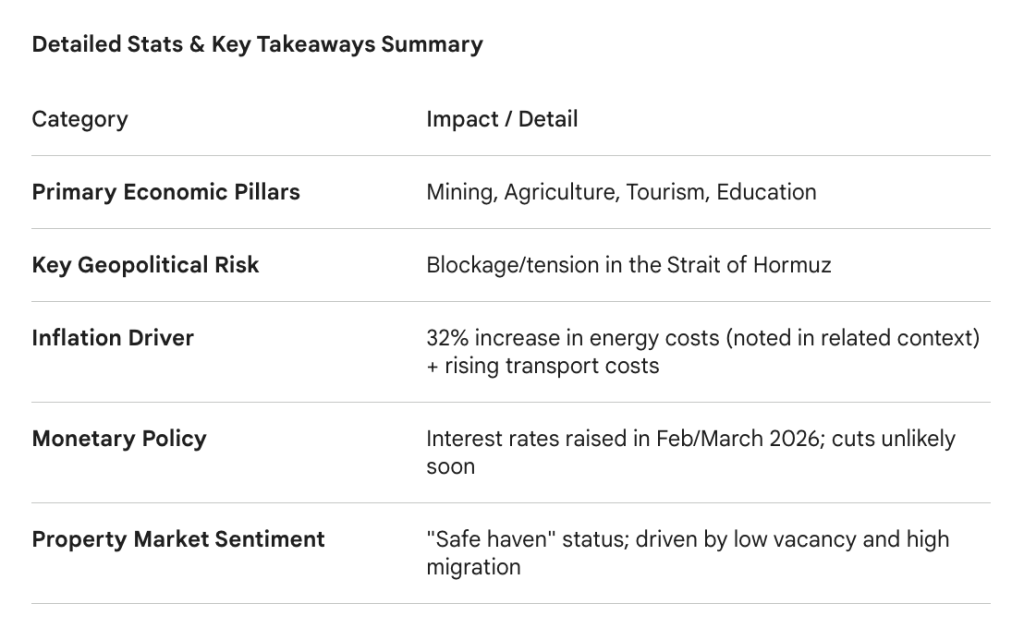

It can definitely feel like Australia is the odd one out. But the key difference is inflation. While the US and Europe appear closer to the end of their inflation fight, Australia is still dealing with inflation that remains stubbornly high and outside the RBA’s comfort zone. Add in a tight labour market, stronger than expected private demand, and the risk that rising fuel and transport costs feed further into everyday prices, and you can see why the RBA still has an upward bias even if it is clearly a close call.

To me, that is the real divergence. The US and Europe appear to be in more of a holding pattern. Australia is not there yet.

In my view, that matters just as much for confidence as it does for repayments. Yes, the direct impact on mortgage holders is real. Borrowing capacity has tightened again and repayment pressure is building. But beyond the numbers, rate rises change how people think and behave. Buyers become more cautious, more budget-conscious, and far less likely to stretch.

Recent commentary around the latest rate move also highlighted what that means on the ground. On an average new mortgage of around $730,000, the latest increase adds another $117 per month in repayments, while borrowing capacity for a median-income household is estimated to have reduced by around $18,000. At the same time, lower quartile property values have continued to outperform, which tells us buyers are still active, but increasingly driven by affordability.

Michael Yardney also touched on an important point this week. Global instability, especially around energy supply and transport costs, has a way of flowing through the whole economy. Even when those issues feel distant, they affect inflation here at home, which then affects interest rates, household budgets, and ultimately confidence in the property market.

My sense is that this keeps buyers engaged, but more measured. It does not mean demand disappears. It simply means decisions take more thought.

Affordability is now a structural issue

This is the other big theme I think we cannot ignore.

Affordability is no longer just about whether rates go up or down. It is increasingly a structural issue tied to the gap between property prices and wage growth. That is what makes the current environment so important, especially for first-home buyers and younger households trying to get started.

According to Brett Warren’s summary of the latest first-home buyer data, entry-level prices have continued to rise well ahead of wages. In practical terms, that means the challenge for many buyers is no longer just servicing a loan. It is getting into the market in the first place.

I think this is one of the reasons we are seeing such strong demand at the more affordable end of the market. Buyers are not necessarily stepping away. They are adjusting. They are looking at different suburbs, different property types, and different strategies just to stay in the market.

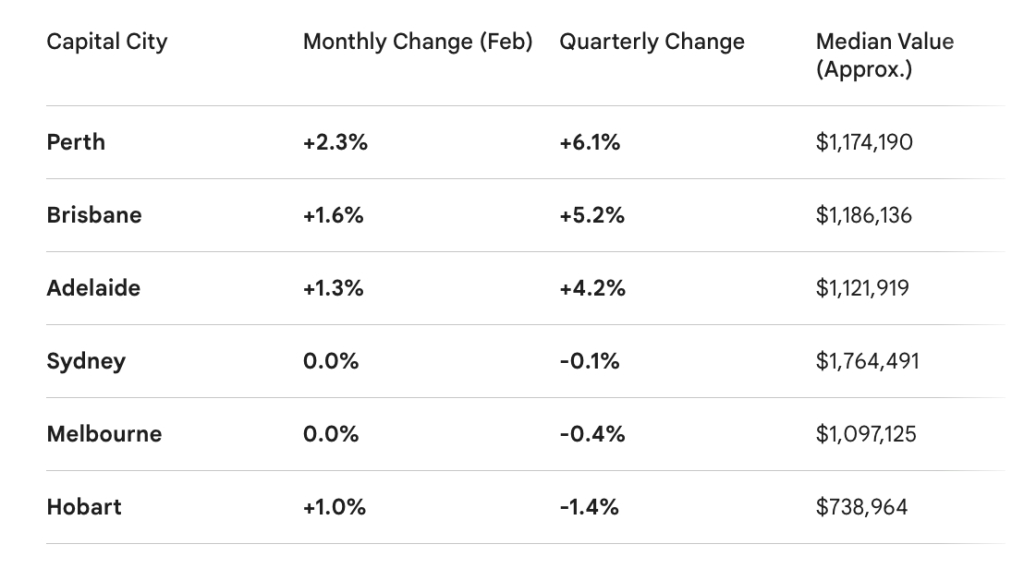

That pattern is showing up nationally as well. The broader market is still resilient, but growth is clearly being led by the more affordable end. In my opinion, that tells us a lot. Buyers still want in, but they are being forced to make sharper, more practical decisions.

It also has a direct effect on the rental market. When first-home buyers stay renters for longer, pressure remains on vacancies and rents. That is one of the reasons rental markets in many parts of the country, including lifestyle regions, are staying tight.

What this means for buyers, sellers, and investors

For buyers, this is a market where preparation matters. Finance needs to be clear, expectations need to be realistic, and compromise is becoming more common. The buyers who are doing well are not necessarily the ones with the biggest budgets. They are the ones who understand their limits and move decisively when the right opportunity appears.

For sellers, I think the message is straightforward. The market is active, but it is no longer forgiving. Buyers are still paying strong prices for the right home, but they are much more value-conscious than they were in easier lending conditions. Overpricing is more likely to hurt momentum now, while strong presentation and smart strategy still make a real difference.

For investors, the environment remains mixed, but still compelling in the right locations. Finance is more expensive, but the supply and demand story remains supportive. Tight rental conditions, population growth, and limited new housing stock are all still working in favour of well-chosen assets.

Sunshine Coast market observations

Here on the Sunshine Coast, I would describe the market as resilient, but increasingly segmented.

Affordable, well-presented homes continue to attract solid attention, particularly where buyers still feel they are getting relative value. That affordability-led trend we are seeing nationally is very relevant locally as well. Buyers are widening their search, considering different dwelling types, and weighing lifestyle against budget much more carefully.

At the upper end, quality still matters enormously. Buyers are active, but they are selective. They want confidence in the property, the location, and the price. That means standout homes can still perform very well, while properties that miss the mark on presentation or pricing can take longer to gain traction.

The rental side of the market remains an important part of the local story too. With affordability pressures keeping some buyers on the sidelines for longer, demand for rentals remains firm. That continues to support investor interest, especially in areas where lifestyle appeal and limited supply combine.

Local perspective and broader takeaway

For me, the key takeaway this week is that the market is still being supported by strong fundamentals, but the pressure points are becoming harder to ignore.

We still have supply constraints, ongoing demand, and strong appeal in lifestyle regions like the Sunshine Coast. But we also have higher rates, tighter borrowing power, rising living costs, and affordability barriers that are changing the way people buy, sell, and invest.

The broader Australian market is also clearly split. Some cities are still recording strong momentum, while others are flattening out as affordability ceilings bite. That kind of divergence matters because it reinforces the idea that buyers are becoming more selective and more value-driven.

There is also the bigger economic backdrop to consider. Australia still has strong structural foundations, but geopolitical instability, energy costs, and inflation pressures are keeping the policy outlook uncertain. Property continues to be seen by many as a relatively stable long-term asset, but confidence is being shaped by much more than just local supply and demand.

So yes, the market is still moving. But it is moving with more thought, more caution, and more selectivity.

That is why I believe good property still stands out. In a market like this, buyers are not chasing everything. They are chasing quality, value, and confidence. And that is exactly why strategy matters more than ever.

If you are considering buying, selling or investing in property on the Sunshine Coast, understanding both the national and local market trends can help you make more confident decisions.

At Martinuzzi Property Group, we’re here to deliver more than a sale. We guide you with radical honesty, exceptional communication, and a stress-free experience, backed by calm confidence, local expertise, and genuine care so you feel informed, supported, and in control from day one to sold.

If you’d like a clear, no pressure view of what your home could achieve in today’s market and what you can do to maximise the outcome, I’m happy to help.

Request Your Free Market Appraisal Today! 👉 Click here to book your appraisal

SUBSCRIBE to stay updated with all latest property insights and news 👉 Click Here to Subscribe

The Sunshine Coast Seller’s Guide to Choosing the Right Agent 👉 Get Your Free Guide Here

Preparing for Settlement: A Seller’s Guide to a Smooth Handover 👉 Download the Guide Here

Sources and Market Data

- Two rate hikes and a potential third set to dampen housing trends

- The Iran War and What It Means for Australia’s Economy and Property Markets

- This week’s Australian Property Market Update

- Australia’s First-Home Buyers Are Facing a New Reality, And It’s Not Just About Interest Rates Anymore